The financial markets – what’s occurring 11 April 2022 The weekly review

My opinion/view of the stock markets is negative/bearish.

Reasons why:

Fed are v serious about anchoring inflation expectations. They do believe, however that a lot of the inflation is caused by supply chain disruptions and the opening up of economies causing wage inflation pressure (many have quit the labour market for good). They have not acknowledge their part in the current inflationary environment, printing money is very Inflationary,

Higher interest rates and higher bond yields will slow the consumer down. They will cost companies more in payments, postpone investments.

Historically, a FED tightening programme has caused a recession (that is the intention, slow down employment to keep wages lower, and take money out of the consumers pocket, through higher mortgage and car loan payments.

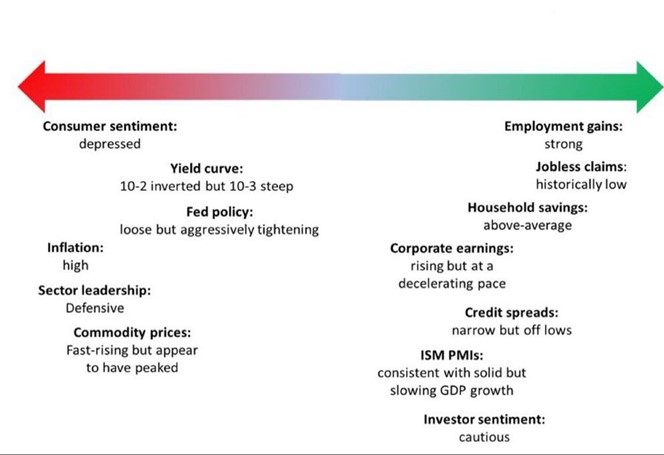

A recession is BAD for stocks and the withdrawal of Bond Buying will mean that fringe cos, like all the recent tech companies will be starved of finance and go bust. This will have a knock on effect on other tech stocks (sell the good to pay for Bad). The increase in funding costs will also affect the over-borrowed. The bond market tends to lead and always be right!!! It is showing higher yields across the curve and is inverted.

The new Bond Market course is available here!!! https://iift.ie/bond-market-trading-investing/

There is also a risk from financial market losses arising from Funds etc long of Bonds at the low rates.

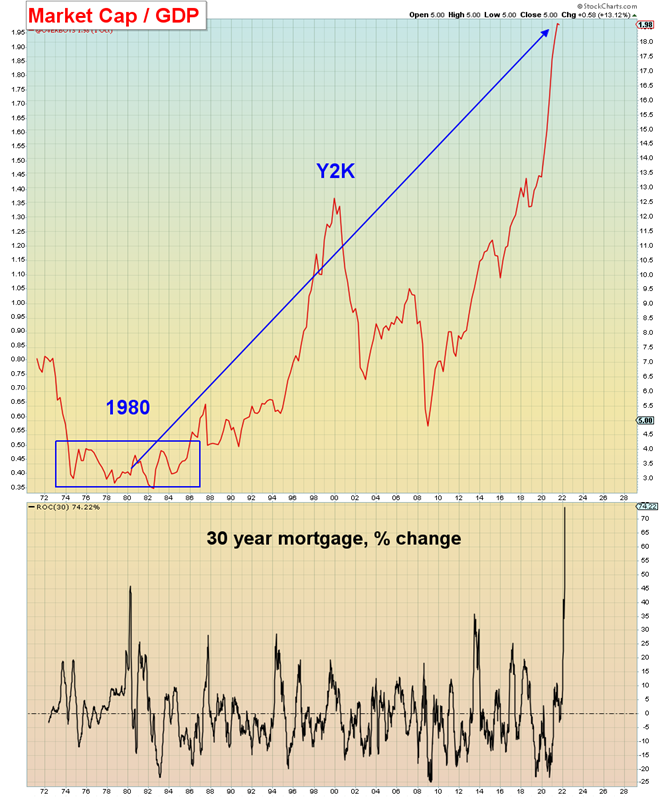

TINA was one of the reasons the stock market rallied since March 2020- there is no alternative (bond yields were so low across the world) investors could only get a return in the stock market. THIS IS NOT THE CASE NOW.

Economy -US

Good ISM numbers midweek were negated by the Hawkish Fed Tone. Brainard gave the stock market “a punch in the nose” saying the FED would withdraw all financial support and Fed Funds Rates would increase by .5% in May and likely in June!!!

CPI and PPI in US due this week. Inflation is likely to be persistently high.

Merrill: “Headline CPI likely surged 1.1% mom in March, while core should rise 0.4% (0.40% unrounded) mom. Yoy rates should accelerate to 8.4% and 6.5%, respectively, which we expect will reflect the peak for yoy inflation.”

Fed watch

Fed speakers last week ruined the bull run. They need to keep Inflation expectations anchored and will increase Fed fund rates regularly. They will stop buying Bonds 60 b mortgage-backed securities and 60b gov/corp bonds.

GOLDMAN’S HATZIUS: I SEE A CHANCE THAT THE FED MAY NEED TO HIKE RATES PAST 4%.

FED’S MESTER: INFLATION IS BEING DRIVEN BY REASONS OTHER THAN MONETARY POLICY. THE FED’S GOAL IS TO PROTECT IT FROM BEING EMBEDDED.

China

Talk of covid lockdowns may not be as extreme as Twitter would have it.

Bonds

“30 year bond bullish sentiment is at 8% bulls. That’s extreme”

Like all markets when everyone is the one way, the market can be squeezed. This is a contrarian indicator and a suggestion that some bond buying could be a good trade.

“Yields on 10-year Treasuries just topped yields on 30-year Treasuries. The yield curve is now inverted from 5s to 30s. The next step is for 2s to surpass 5s. The market clearly sees recession but is still oblivious to #inflation. Inflation won’t return to 2%. It will exceed 10%!”

Geopolitics

As mentioned, many times, the further in time we move from a major incident the less effect it has on markets.

Easter trading opening hours

Tomorrow: CPI *Wed: PPI *Thur: Retail sales, import prices, UMich sentiment survey

Stock market

The usual cross currents.

“I’m increasingly convinced we’re in a roughly 18-month bear market since January’s peak that by the fall of 2023 will take the S&P down at LEAST 35% from its ATH (to 3130) and more likely 50% (2400). Look at the bears of 1973-74, 2000-02 & 2007-09.”

STRONG STUFF HERE………..

My chart guy says

After a 500 point rally, what came next isn’t shocking: #ES_F is retracing. Bigger pattern suggests highs not in (4680 target) but risk of more pullback first Plan next week: Unless bulls can pop above 4500 to mark a low, dip to 4420, 4385 is 1st $SPX

https://www.investing.com/earnings-calendar/

EARNINGS SEASON STARTS THIS WEEK

BANKS RESULTS OUT ALL WEEK

Conclusion

Seasonally still positive, but interest rates and bond yields cast a shadow.

Earnings will have to be amazing to maintain these high prices, any weakness will lead to sell off/profit taking.

Colin 01-6644034 0851722729

Risk management is vital.