As markets brace for a pivotal week, investors will be closely monitoring inflation indicators and trade policy shifts. The U.S. Personal Consumption Expenditures (PCE) index is set to be released, providing key insights into inflation trends, particularly as concerns over tariffs resurface under Trump 2.0. The Federal Reserve is expected to maintain its pause on interest rates, though market speculation about potential rate cuts continues to drive volatility.

Japanese inflation data and a Bank of Japan (BoJ) decision could significantly impact global sentiment, particularly as the yen fluctuates amid expectations of central bank policy shifts. The U.S. job market data will also take center stage, influencing the dollar’s trajectory and shaping investor sentiment. With King Dollar gaining momentum, emerging markets may face increased pressure.

In Europe, markets are digesting the fallout from Trump’s tariff proposals, which have already led to a drop in European equities. Major food companies like Diageo, Unilever, and PepsiCo could face headwinds, while Cairn Homes’ strong performance suggests resilience in the housing sector. Meanwhile, the S&P 500 will be in focus as investors weigh liquidity trends ahead of a potential holiday lull.

With increased uncertainty surrounding central bank actions, inflation fears, and trade tensions, investors should brace for volatility. Those with exposure to affected sectors, such as consumer goods and industrials, should consider risk management strategies, while defensive assets like gold remain a hedge against market turbulence.

Stock Market Indices Table & Private Investor Commentary

Stock Market Indices Performance

| Index | Last Close | Change in Last 7 Days | Change in Last 30 Days |

|---|---|---|---|

| S&P 500 | 5,956 | -161 | -112 |

| Dow Jones | 43,433 | -744 | -1,417 |

| Nasdaq | 19,075 | -887 | -658 |

| FTSE | 8,731 | 68 | 198 |

| DAX | 22,794 | 479 | 1,364 |

| Hang Seng | 23,788 | 1,211 | 3,563 |

| VIX | 19 | 3 | 3 |

| Gold | 2,931 | -26 | 136 |

| Copper | 5 | 0 | 0 |

| Silver | 33 | -1 | 2 |

| Oil | 69 | -4 | -5 |

Investor Commentary

The past week has been turbulent for U.S. equities, with the S&P 500, Dow Jones, and Nasdaq all declining amid inflation fears and renewed tariff concerns. The tech-heavy Nasdaq took a significant hit (-887 points), reflecting investor caution as higher inflation could delay Fed rate cuts. European stocks showed mixed performance; while the FTSE posted gains, concerns over Trump’s trade policies led to declines in other indices.

Meanwhile, the Hang Seng surged, benefiting from increased liquidity and expectations of economic recovery in China. The DAX also rallied, reflecting market optimism following a conservative political win in Germany. Volatility remains elevated (VIX up by 3), indicating that uncertainty persists.

Commodities were mixed—gold lost ground, reflecting short-term shifts in risk appetite, while oil continued to decline, likely due to concerns over global demand. Investors should remain cautious, particularly in sectors exposed to geopolitical risks, and consider defensive positioning amid upcoming inflation reports.

Sector Performance Chart & Commentary

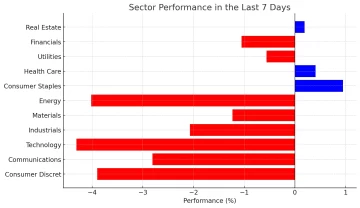

Sector Performance in the Last 7 Days

The past week has seen significant declines across major sectors, with Technology (-4.31%) and Energy (-4.02%) leading the downturn. This aligns with broader market concerns over tariffs, inflation, and Fed policy uncertainty. Defensive sectors such as Consumer Staples (+0.95%) and Health Care (+0.41%) saw modest gains, reflecting investor caution. The market remains highly sensitive to upcoming economic reports.