Introduction

As we approach the final quarter of 2024, the global economic environment is characterized by a mix of cautious optimism and underlying risks. Investors face a complex landscape where central bank policies, fiscal challenges, geopolitical tensions, and fluctuating commodity prices intertwine, shaping the trajectory of markets. This commentary provides a detailed analysis of the current macroeconomic conditions, offering insights into investment strategies that align with these dynamics.

Monetary Policy: Tightening with Caution

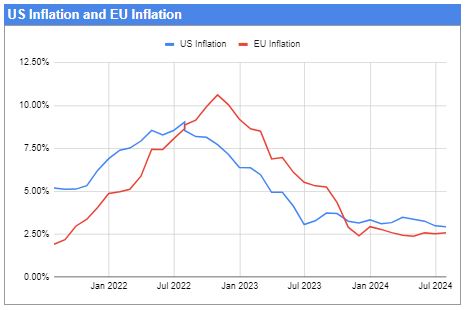

The U.S. Federal Reserve remains focused on its primary objectives of maintaining maximum employment and achieving a stable inflation rate. As of mid-2024, the Federal Reserve has kept the federal funds rate in the range of 5.25% to 5.50%, reflecting its commitment to bringing inflation down to its 2% target. The inflation rate has moderated significantly from its peak of 8.54% in July 2022 to 2.92% by July 2024, signaling progress but still above the Fed’s target.

Table 1: U.S. Inflation and Interest Rates

| Date | US Inflation | US Interest Rate |

|---|---|---|

| Jul 2024 | 2.92% | 5.25% – 5.50% |

| Jan 2024 | 3.10% | 5.50% |

| Jul 2023 | 3.27% | 5.50% |

The European Central Bank (ECB) is also maintaining a tight monetary policy, with its interest rate at 4.25% as of July 2024. The ECB’s focus remains on achieving its 2% inflation target, with inflation in the Eurozone moderating to 2.58%, down from the higher levels seen in previous years.

Investment Strategy Example: In this high-interest-rate environment, investors may find fixed-income securities, such as U.S. Treasuries and high-quality corporate bonds, attractive due to their relatively stable returns. Additionally, sectors like financials, which benefit from higher interest rates, and consumer staples, which provide stable cash flows, could offer robust investment opportunities.

Fiscal Policy: A Shift Toward Restraint

On the fiscal side, the U.S. government is grappling with a growing fiscal deficit, which nearly doubled to 7.4% of GDP in 2023. This expansion was driven by lower tax revenues and sustained government spending. In response, 2024 is expected to see a shift toward a more restrained fiscal policy aimed at reducing the deficit. However, this shift may act as a slight drag on economic growth, especially as the effects of previous fiscal stimulus begin to wane.

Table 2: U.S. GDP Growth

| Date | US GDP (Trillion USD) |

|---|---|

| Jun 2024 | 28.71 |

| Jun 2023 | 27.19 |

| Jun 2022 | 25.78 |

The slowing pace of GDP growth, combined with tightening fiscal conditions, suggests that economic expansion may become more moderate in the near term. This environment requires investors to focus on sectors that are less sensitive to economic cycles, such as healthcare and utilities, which tend to provide stable returns even during periods of slower growth.

Investment Strategy Example: Investors might consider increasing their exposure to defensive sectors like healthcare, which typically exhibits resilience during economic downturns. Additionally, infrastructure-related investments, such as those in utilities or transportation, could benefit from ongoing government spending on critical infrastructure projects, even amid broader fiscal tightening.

Geopolitical Risks: A Persistent Threat

Geopolitical risks continue to pose significant challenges to the global economy. The ongoing Ukraine-Russia conflict remains a key driver of uncertainty, particularly in terms of its impact on global energy markets and food security. The conflict has led to disruptions in Ukrainian agricultural exports and contributed to volatility in energy prices.

Table 3: Commodity Prices

| Commodity | Last Close | Change in Last 7 Days | Change in Last 30 Days |

|---|---|---|---|

| Gold | 2,560 | 14 | 87 |

| Oil | 76 | 1 | -2 |

U.S.-China relations also remain tense, with potential risks to global trade and supply chains, particularly if tensions over Taiwan escalate into military conflict. Such an outcome could disrupt global stability, with far-reaching consequences for markets and supply chains.

In the Middle East, ongoing instability, particularly around Iran’s nuclear ambitions, poses additional risks to global energy supplies. The region’s significance in global oil production means that any escalation in tensions could lead to sharp increases in oil prices, impacting inflation and economic growth worldwide.

Investment Strategy Example: Given these geopolitical risks, commodities such as gold and oil are likely to remain attractive as safe-haven assets. Additionally, defense sector stocks, such as Lockheed Martin (LMT) and Raytheon Technologies (RTX), could benefit from increased defense spending in response to heightened global tensions.

Corporate Earnings and Consumer Sentiment

Corporate earnings in the U.S. have shown resilience, with S&P 500 earnings reaching 191.39 in March 2024, up from 175.17 in March 2023. This growth in earnings reflects the strength of the U.S. corporate sector, even as the economy faces headwinds from higher interest rates and fiscal challenges.

Table 4: S&P 500 Corporate Earnings

| Date | S&P 500 Corporate Earnings |

|---|---|

| Mar 2024 | 191.39 |

| Mar 2023 | 175.17 |

However, consumer sentiment has softened slightly, with the U.S. Consumer Sentiment Index dipping to 67.80 in August 2024, down from 69.40 a year earlier. This decline reflects consumer concerns about inflation and economic uncertainty, which could weigh on consumer spending in the near term.

Table 5: U.S. Consumer Sentiment

| Date | US Consumer Sentiment |

|---|---|

| Aug 2024 | 67.80 |

| Aug 2023 | 69.40 |

| Aug 2022 | 58.20 |

Investment Strategy Example: Investors should consider focusing on companies with strong earnings growth and robust balance sheets, particularly in sectors such as technology and consumer goods. Technology giants like Apple (AAPL) and Microsoft (MSFT) continue to demonstrate resilience and growth potential, making them attractive investments even in uncertain economic conditions.

Global Trade and Productivity Trends

The global trade environment in 2024 remains challenging, influenced heavily by the geopolitical tensions discussed earlier. The U.S. trade balance continues to show a significant deficit, with the June 2024 figure at -$73.11 billion, reflecting ongoing challenges in export competitiveness and a strong U.S. dollar.

Table 6: U.S. Trade Balance

| Date | US Trade Balance (Billion USD) |

|---|---|

| Jun 2024 | -73.11 |

| Jun 2023 | -64.81 |

Productivity in the U.S. has shown modest improvement, with productivity growth reaching 2.30% in June 2024. This marks a positive shift from previous years, where productivity growth had stagnated or declined. Improved productivity is crucial for sustaining economic growth, particularly in an environment where labor markets are tight and inflationary pressures persist.

Table 7: U.S. Productivity Growth

| Date | US Productivity Growth |

|---|---|

| Jun 2024 | 2.30% |

| Jun 2021 | -0.10% |

Investment Strategy Example: In light of these trade and productivity trends, investors might consider companies that are leaders in automation and technology, which can enhance productivity. For example, investing in companies like NVIDIA (NVDA) and Amazon (AMZN), which are at the forefront of artificial intelligence and automation, could be beneficial as these technologies play a key role in driving future productivity gains.

Housing Market: Cooling Amidst High Rates

The U.S. housing market has shown signs of cooling, with housing starts declining to 1.24 million units in July 2024 from 1.47 million units in July 2023. This decline reflects the impact of higher interest rates, which have increased the cost of mortgages and dampened housing demand.

Table 8: U.S. Housing Starts

| Date | US Housing Starts (Million Units) |

|---|---|

| Jul 2024 | 1.24 |

| Jul 2023 | 1.47 |

Investment Strategy Example: Given the cooling housing market, real estate investment trusts (REITs) focused on sectors less sensitive to interest rate changes, such as healthcare or industrial properties, may offer attractive investment opportunities. Additionally, companies involved in home improvement, such as Home Depot (HD) and Lowe’s (LOW), may continue to perform well as homeowners invest in renovating existing properties rather than purchasing new ones.

Conclusion

The global macroeconomic environment in 2024 is characterized by a mix of opportunities and challenges. While monetary and fiscal policies remain tight, the resilience of corporate earnings, along with the potential for technological advancements, provides a basis for cautious optimism. Geopolitical risks continue to loom large, necessitating a focus on diversification and defensive strategies.

Investors should maintain a diversified portfolio that balances exposure to high-quality equities, fixed income, commodities, and alternative assets. By staying informed and adapting to changing conditions, investors can navigate the uncertainties of the current macroeconomic landscape while positioning for long-term success.